What is interest?

In the most simplest of terms, interest can be defined as the cost of borrowing money or the rate paid for a deposit. Different banks adopt different strategies of providing interest and it can have a drastic effect on one’s income.

Simple interest

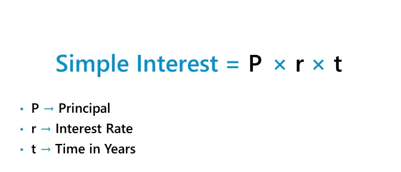

Simple Interest is calculated on the principal amount of the original loan. The formula for calculating simple interest is given below:

Thus, if the interest rate is 5% on a loan of Rs 1,00,000 the total interest after 3 years will be Rs15,000.

Compound interest

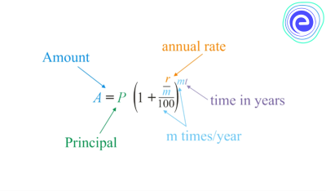

Compound interest is calculated on the principal amount and the accumulated interest of previous periods. This is why it is regarded as interest on interest. The formula for calculating compound interest is given below:

Thus if the interest rate is 5% charged annually for 3 years on the principal amount of 1,00,000 the total interest will be Rs 15,762.5. It is evident that compound interest yields higher revenue than its simple counterpart.

Compounding periods

The number of compounding periods significantly affect the resulting compound interest. Generally, higher the number of compounding periods, more is the amount of compound interest. For every Rs 100,000 invested over a certain period of time, the compound interest charged at 5% semi-annually will be more than compound interest charged 10% annually.

Time Period of Time

Since money is not “free” but has a cost in terms of interest payable, it follows that a dollar today is worth more than a dollar in the future. This concept is known as time value of money and forms the basis for advanced financial techniques such as discounted cash flow. The opposite of compounding is discounting. It can be considered as the reciprocal of interest rate and is the factor by which a future value must be multiplied to get the present value.

Rule of 72

The rule of 72 determines the time in which the value of investment will double at a given rate of interest. It is calculated by dividing 72 by the interest rate.

Eg. If the interest rate is 8%, then the principal amount will double in 9 years as 72/i= 72/8= 9.

Impact of Interest Rates on the global economy

Change in interest rates can have both positive and negative effects on the economy. Banks raise interest rates when the economy is flourishing and decrease rates when it is sluggish. Higher interest rates decrease the spending capability of the consumer as more of their money goes into paying back loans and getting rid of financial debt. Lower the interest rate, the more willing people are to borrow money to make big purchases, such as houses or cars. In general, rising interest rates curb inflation and decreased rates encourage the increase in prices of goods and services.